-

America’s Car-Mart Reports Second Quarter Fiscal Year 2025 Results

Source: Nasdaq GlobeNewswire / 05 Dec 2024 07:30:43 America/New_York

ROGERS, Ark., Dec. 05, 2024 (GLOBE NEWSWIRE) -- America’s Car-Mart, Inc. (NASDAQ: CRMT) (“we,” “Car-Mart” or the “Company”), today reported financial results for the second quarter ended October 31, 2024.

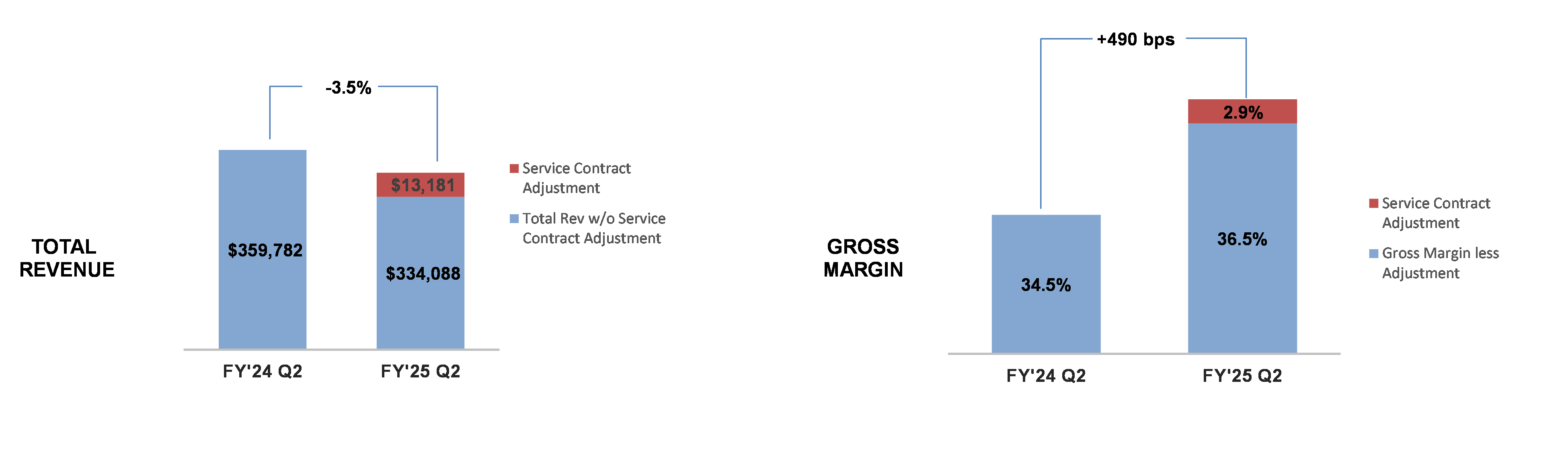

Second Quarter Key Highlights (FY’25 Q2 vs. FY’24 Q2, unless otherwise noted) - Total revenue was $347.3 million1, down 3.5%

- Interest income increased $2.1 million, up 3.6%

- Total collections increased 3.3% to $173.8 million

- Gross margin increased to 39.4%1

- Adjustment to allowance for credit loss to 24.72%, down from 25.0% sequentially

- Net charge-offs as a % of average finance receivables were 6.6% vs. 7.2%

- Interest expense increased $1.5 million, or 8.8%

- Diluted earnings per share of $0.611 vs. loss per share of $4.30

President and CEO Doug Campbell commentary:

“As we navigated industry and economic pressures, we made strategic decisions to ensure we exited stronger and better positioned to profitably grow our market share during the second half of the fiscal year. I am pleased with our progress, as we continue to benefit from our enhanced underwriting or loan origination system (LOS). We improved deal structures, generated higher down payments, and benefited from higher collections and gross margins. We continue to focus on improving affordability for customers by reducing the average retail price. We’re closely managing expenses during ongoing implementation of technology upgrades to strengthen our operations. We believe Car-Mart is well positioned for future growth and profitability.”

1 During the second quarter of fiscal year 2025, the Company made an adjustment after a performance analysis on our service contract program leading to an accounting change reducing the estimated revenue recognition period. This analysis revealed that our customers reach the mileage portion of their service contract 25% sooner than the expiration of the contract term. Because of this, we reduced our revenue recognition period to better match the time of usage by the consumer. This resulted in an acceleration of deferred service contract revenue on outstanding contracts of $13.2 million this quarter and will result in faster revenue recognition in subsequent periods. Excluding the impact of this accounting adjustment, the Company’s adjusted loss per share for the quarter was $0.24. Calculation of this non-GAAP financial measure and a reconciliation to the most directly comparable GAAP measure are included in the tables accompanying this release.

Second Quarter Fiscal Year 2025 Key Operating Metrics Dollars in thousands, except per unit data. Dollar and percentage changes may not recalculate due to rounding. Charts may not be to scale.

Second Quarter Business Review Note: Discussions in each section provide information for the second quarter of fiscal year 2025 compared to the second quarter of fiscal year 2024, unless otherwise noted.

TOTAL REVENUE – A 3.5% decline in revenue was primarily driven by a decrease in retail units sold. The decline in revenue was partially offset by an increase in interest income and a $13.2 million benefit in service contract revenue. The increase in service contract revenue was a result of a performance analysis on our service contract program resulting in an accounting change reducing the estimated revenue recognition period.

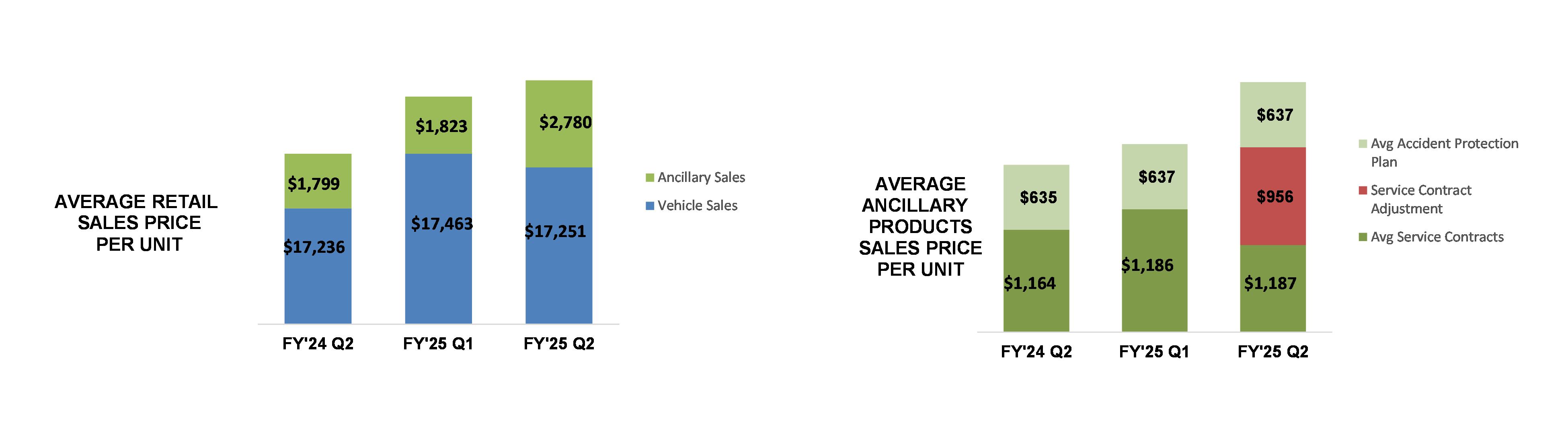

SALES – Sales were 13,784 units vs. 15,162 units. The 9.1% reduction in sales volumes for the quarter was impacted by lower volumes in September, due partially to weather events in various markets. The Company also closed two underperforming dealerships during the quarter. The average vehicle retail sales price, excluding ancillary products, decreased to $17,251, reflecting a $212 decrease in the vehicle retail sales price when viewed sequentially, and for the second quarter in a row.

GROSS PROFIT – Gross profit margin as a percentage of sales was 39.4%, including 290 bps benefit from the impact of the service contract accounting change in estimate for revenue recognition. This accounting change will have a positive effect going forward on gross margin. Absent this change, adjusted gross margin (non-GAAP)2 as a percentage of sales for the quarter was 36.5%, which is an improvement of 200 bps over the prior year quarter and 150 bps sequentially. Our initiatives in improving wholesale results and pricing improvements are reflected in these improved margins.

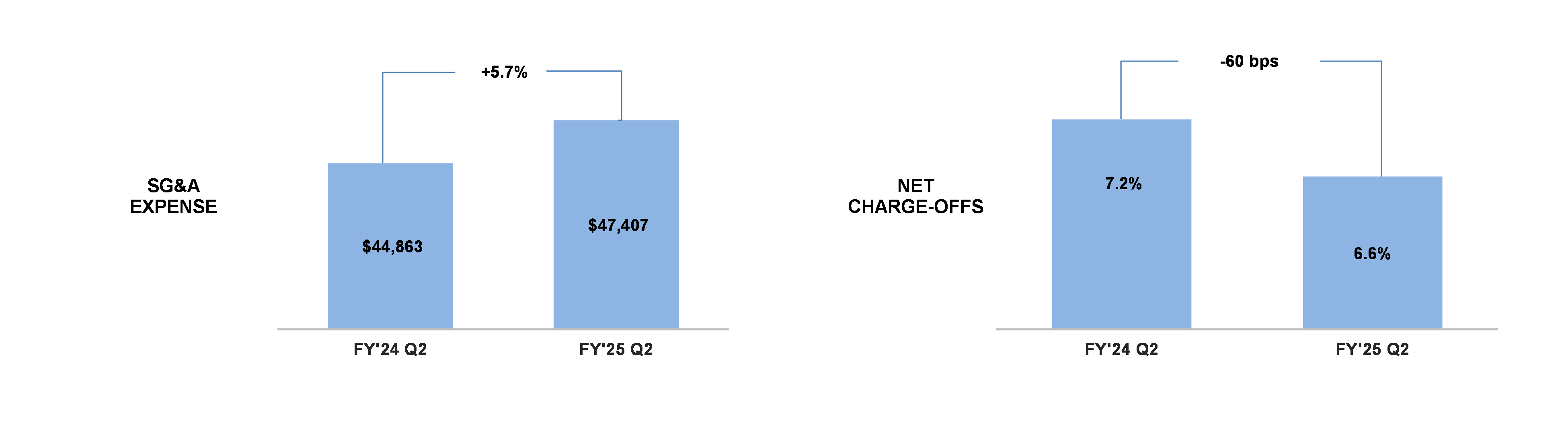

NET CHARGE-OFFS – Net charge-offs as a percentage of average finance receivables improved to 6.6% compared to 7.2%. On a relative basis, we saw improvements in the frequency of losses and a small increase in the severity of loss. We are seeing the severity of loss taper off when looking at loss per unit sequentially.

ALLOWANCE FOR CREDIT LOSSES – The allowance for credit loss as a percentage of finance receivables, net of deferred revenue and pending accident protection plan claims, decreased from 25.00% at July 31, 2024, to 24.72% at October 31, 2024. The primary driver of this change was favorable performance in loans originated under our LOS (our improved underwriting system) and the improvements it is driving in our historical loss rates. As of October 31, 2024, approximately 50% of the outstanding portfolio balance was originated under the Company’s enhanced LOS. Delinquencies (accounts over 30 days past due) improved by 10 bps to 3.5% of finance receivables as of October 31, 2024, and remained flat sequentially.

UNDERWRITING – Average down payments improved 30 bps to 5.2%. The average originating term was 44.2 months, essentially flat compared to the prior year quarter and a slight reduction sequentially. The Company continues to focus on improving deal structures particularly within the underlying credit tiers of customers, which the Company expects to strengthen the performance of the portfolio going forward. Please see the table and supplemental material for Cash-on-Cash returns.

SG&A EXPENSE – SG&A expense was up 5.7% to $47.4 million from $44.9 million. The Company’s last two acquisitions completed since last year drove $2.1 million of the increase and the remainder was related to stock compensation increases. We had favorable declines in payroll and payroll-related costs from prior expense management actions which we are pleased with. SG&A per customer was $459 compared to $429, but we expect this increase to flatten out as the acquisition customer bases grow. The acquisitions completed last year are projected to add an additional 5,000-6,000 more accounts over the next 18-24 months.

LEVERAGE & LIQUIDITY – Debt to finance receivables and debt, net of cash, to finance receivables (non-GAAP)2 were 51.8% and 43.0%, compared to 52.6% and 46.0%, respectively, at the end of the prior year. During the quarter, the Company completed an underwritten public equity offering and a private asset-backed securitization offering resulting in proceeds, net of issuance costs, of $73.8 million and $297.9 million, respectively, which were used primarily to pay down existing debt. During the quarter, the Company grew finance receivables by $8.5 million, increased inventory by $7.6 million, and purchased fixed assets of $1.4 million, with a $49.6 million decrease in debt, net of cash. As of October 31, 2024, the Company had $107.4 million in outstanding borrowings under its revolving line of credit.

ANNUAL CASH-ON-CASH RETURNS – The Company continues to generate solid cash-on-cash returns.

The following table sets forth the actual and projected cash-on-cash returns as of October 31, 2024, for the Company’s finance receivables by origination year. The return percentages provided for contracts originated in fiscal years 2017 through 2020 reflect the Company’s actual cash-on-cash returns.

Cash-on-Cash Returns3 Loan Origination

YearPrior Quarter

ProjectedCurrent Quarter

Actual/ProjectedVariance % of A/R

RemainingFY2017 * 61.1% * 0.0% FY2018 * 67.6% * 0.0% FY2019 * 70.0% * 0.0% FY2020 * 73.6% * 0.1% FY2021 72.5% 72.4% -0.1% 1.5% FY2022 54.9% 53.8% -1.1% 9.0% FY2023 49.1% 47.1% -2.0% 23.6% FY2024 64.4% 62.9% -1.5% 52.7% FY2025 72.4% 72.3% -0.1% 89.7% * 2017 - 2020 Pools' Current Projection reflects actual cash-on-cash returns 2 Calculation of this non-GAAP financial measure and a reconciliation to the most directly comparable GAAP measure are included in the tables accompanying this release.

3 “Cash-on-cash returns” represent the return on cash invested by the Company in the vehicle finance loans the Company originates and is calculated with respect to a pool of loans (or finance receivables) by dividing total “cash in” less “cash out” by total “cash out” with respect to such pool. “Cash in” represents the total cash the Company expects to collect on the pool of finance receivables, including credit losses. This includes down-payments, principal and interest collected (including special and seasonal payments) and the fair market value of repossessed vehicles, if applicable. “Cash out” includes purchase price paid by the Company to acquire the vehicle (including reconditioning and transportation costs), and all other post-sale expenses as well as expenses related to our ancillary products. The calculation assumes estimates on expected credit losses net of fair market value of repossessed vehicles and the related timing of such losses as well as post sales repair expenses and special payments. The Company evaluates and updates expected credit losses quarterly. The credit quality of each pool is monitored and compared to prior and initial forecasts and is reflected in our on-going internal cash-on-cash projections.

Key Operating Results Three Months Ended October 31, 2024 2023 % Change Operating Data: Retail units sold 13,784 15,162 (9.1) % Average number of stores in operation 154 154 - Average retail units sold per store per month 29.8 32.8 (9.1) Average retail sales price $ 20,031 $ 19,035 5.2 Total gross profit per retail unit sold $ 8,166 $ 6,835 19.5 Total gross profit percentage 39.4% 34.5% Same store revenue growth (8.4)% 2.6% Net charge-offs as a percent of average finance receivables 6.6% 7.2% Total collected (principal, interest and late fees), in thousands $ 173,778 $ 168,282 3.3 Average total collected per active customer per month $ 560 $ 533 5.1 Average percentage of finance receivables-current (excl. 1-2 day) 81.8% 80.4% Average down-payment percentage 5.2% 4.9% Six Months Ended October 31, 2024 2023 % Change Operating Data: Retail units sold 28,175 31,074 (9.3) % Average number of stores in operation 155 155 - Average retail units sold per store per month 30.3 33.4 (9.3) Average retail sales price $ 19,650 $ 18,914 3.9 Total gross profit per retail unit sold $ 7,568 $ 6,801 11.3 Total gross profit percentage 37.2% 34.6% Same store revenue growth (8.2)% 5.4% Net charge-offs as a percent of average finance receivables 13.0% 13.1% Total collected (principal, interest and late fees), in thousands $ 346,650 $ 334,029 3.8 Average total collected per active customer per month $ 561 $ 534 5.0 Average percentage of finance receivables-current (excl. 1-2 day) 82.1% 80.4% Average down-payment percentage 5.2% 4.9% Period End Data: Stores open 154 153 0.7 % Accounts over 30 days past due 3.5% 3.6% Active customer count 103,336 104,596 (1.2) Principal balance of finance receivables (in thousands) $ 1,473,794 $ 1,463,398 0.7 Weighted average total contract term 48.2 47.3 1.9 Conference Call and Webcast The Company will hold a conference call to discuss its quarterly results on Thursday, December 5, 2024, at 9 am ET. Participants may access the conference call via webcast using this link: Webcast Link. To participate via telephone, please register in advance using this Registration Link. Upon registration, all telephone participants will receive a one-time confirmation email detailing how to join the conference call, including the dial-in number along with a unique PIN that can be used to access the call. All participants are encouraged to dial in 10 minutes prior to the start time. A replay and transcript of the conference call and webcast will be available on-demand for 12 months.

About America’s Car-Mart, Inc. America’s Car-Mart, Inc. (the “Company”) operates automotive dealerships in 12 states and is one of the largest publicly held automotive retailers in the United States focused exclusively on the “Integrated Auto Sales and Finance” segment of the used car market. The Company emphasizes superior customer service and the building of strong personal relationships with its customers. The Company operates its dealerships primarily in smaller cities throughout the South-Central United States, selling quality used vehicles and providing financing for substantially all of its customers. For more information about America’s Car-Mart, including investor presentations, please visit our website at www.car-mart.com.

Non-GAAP Financial Measures This news release contains financial information determined by methods other than in accordance with generally accepted accounting principles (GAAP). We present adjusted diluted earnings (loss) per share, adjusted gross margin as a percentage of finance receivables, and total debt, net of total cash, to finance receivables, each a non-GAAP measure, as supplemental measures of our performance. We believe adjusted diluted earnings (loss) per share and adjusted gross margin as a percentage of sales are useful measures of our operating results because they exclude the impacts of an adjustment that is not indicative of our underlying operating performance. We believe total debt, net of total cash, to finance receivables is a useful measure to monitor leverage and evaluate balance sheet risk. These measures should not be considered in isolation or as a substitute for reported GAAP results because they may include or exclude certain items as compared to similar GAAP-based measures, and such measures may not be comparable to similarly-titled measures reported by other companies. We strongly encourage investors to review our consolidated financial statements included in publicly filed reports in their entirety and not rely solely on any one, single financial measure or communication. The most directly comparable GAAP financial measure, as well as a reconciliation to the comparable GAAP financial measure, for non-GAAP financial measures are presented in the tables of this release.

Forward-Looking Statements This news release contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements address the Company’s future objectives, plans and goals, as well as the Company’s intent, beliefs and current expectations and projections regarding future operating performance and can generally be identified by words such as “may,” “will,” “should,” “could,” “expect,” “anticipate,” “intend,” “plan,” “project,” “foresee,” and other similar words or phrases. Specific events addressed by these forward-looking statements may include, but are not limited to:

- operational infrastructure investments;

- same dealership sales and revenue growth;

- customer growth and engagement;

- gross profit percentages;

- gross profit per retail unit sold;

- business acquisitions;

- inventory acquisition, reconditioning, transportation, and remarketing;

- technological investments and initiatives;

- future revenue growth;

- receivables growth as related to revenue growth;

- new dealership openings;

- performance of new or existing dealerships;

- interest rates;

- future credit losses;

- the Company’s collection results, including but not limited to collections during income tax refund periods;

- cash-on-cash returns from the collection of contracts originated by the Company

- seasonality; and

- the Company’s business, operating and growth strategies and expectations.

These forward-looking statements are based on the Company’s current estimates and assumptions and involve various risks and uncertainties. As a result, you are cautioned that these forward-looking statements are not guarantees of future performance, and that actual results could differ materially from those projected in these forward-looking statements. Factors that may cause actual results to differ materially from the Company’s projections include, but are not limited to:

- general economic conditions in the markets in which the Company operates, including but not limited to fluctuations in gas prices, grocery prices and employment levels and inflationary pressure on operating costs;

- the availability of quality used vehicles at prices that will be affordable to our customers, including the impacts of changes in new vehicle production and sales;

- the ability to leverage the Cox Automotive services agreement to perform reconditioning and improve vehicle quality to reduce the average vehicle cost, improve gross margins, reduce credit loss, and enhance cash flow;

- the availability of credit facilities and access to capital through securitization financings or other sources on terms acceptable to us, and any increase in the cost of capital, to support the Company’s business;

- the Company’s ability to underwrite and collect its contracts effectively, including whether anticipated benefits from the Company’s recently implemented loan origination system are achieved as expected or at all;

- competition;

- dependence on existing management;

- ability to attract, develop, and retain qualified general managers;

- changes in consumer finance laws or regulations, including but not limited to rules and regulations that have recently been enacted or could be enacted by federal and state governments;

- the ability to keep pace with technological advances and changes in consumer behavior affecting our business;

- security breaches, cyber-attacks, or fraudulent activity;

- the ability to identify and obtain favorable locations for new or relocated dealerships at reasonable cost;

- the ability to successfully identify, complete and integrate new acquisitions;

- the occurrence and impact of any adverse weather events or other natural disasters affecting the Company’s dealerships or customers; and

- potential business and economic disruptions and uncertainty that may result from any future public health crises and any efforts to mitigate the financial impact and health risks associated with such developments.

Additionally, risks and uncertainties that may affect future results include those described from time to time in the Company’s SEC filings. The Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the dates on which they are made.

Contact for information Vickie Judy, CFO

479-464-9944

Investor_relations@car-mart.comAmerica's Car-Mart, Inc. Consolidated Results of Operations (Amounts in thousands, except per share data) As a % of Sales Three Months Ended Three Months Ended October 31, October 31, 2024 2023 % Change 2024 2023 Statements of Operations: Revenues: Sales(4) $ 285,774 $ 300,400 (4.9 ) % 100.0 % 100.0 % Interest income 61,495 59,382 3.6 21.5 19.8 Total(4) 347,269 359,782 (3.5 ) 121.5 119.8 . Costs and expenses: Cost of sales(4) 173,215 196,763 (12.0 ) 60.6 65.5 Selling, general and administrative 47,407 44,863 5.7 16.6 14.9 Provision for credit losses 99,522 135,395 (26.5 ) 34.8 45.1 Interest expense 18,042 16,582 8.8 6.3 5.5 Depreciation and amortization 1,926 1,696 13.6 0.7 0.6 Loss on disposal of property and equipment 41 74 (44.6 ) - - Total(4) 340,153 395,373 (14.0 ) 119.0 131.6 Income (loss) before taxes 7,116 (35,591 ) 2.5 (11.8 ) Provision (benefit) for income taxes 2,017 (8,128 ) 0.7 (2.7 ) Net income (loss) $ 5,099 $ (27,463 ) 1.8 (9.1 ) Dividends on subsidiary preferred stock $ (10 ) $ (10 ) Net income (loss) attributable to common shareholders $ 5,089 $ (27,473 ) Earnings per share: Basic $ 0.62 $ (4.30 ) Diluted $ 0.61 $ - Weighted average number of shares used in calculation: Basic 8,147,971 6,386,208 Diluted 8,292,459 6,386,208 America's Car-Mart, Inc.

Consolidated Results of Operations(Amounts in thousands, except per share data) As a % of Sales Six Months Ended Six Months Ended October 31, October 31, 2024 2023 % Change 2024 2023 Statements of Operations: Revenues: Sales(4) $ 573,022 $ 610,737 (6.2 ) % 100.0 % 100.0 % Interest income 122,010 115,838 5.3 21.3 19.0 Total(4) 695,032 726,575 (4.3 ) 121.3 119.0 Costs and expenses: Cost of sales(4) 359,785 399,410 (9.9 ) 62.8 65.4 Selling, general and administrative 94,118 91,333 3.0 16.4 15.0 Provision for credit losses 194,945 231,718 (15.9 ) 34.0 37.9 Interest expense 36,354 30,856 17.8 6.3 5.1 Depreciation and amortization 3,810 3,389 12.4 0.7 0.6 Loss on disposal of property and equipment 87 240 (63.8 ) - - Total(4) 689,099 756,946 (9.0 ) 120.2 124.0 Income (loss) before taxes 5,933 (30,371 ) 1.0 (5.0 ) Provision (benefit) for income taxes 1,798 (7,094 ) 0.3 (1.2 ) Net income (loss) $ 4,135 $ (23,277 ) 0.7 (3.8 ) Dividends on subsidiary preferred stock $ (20 ) $ (20 ) Net income (loss) attributable to common shareholders $ 4,115 $ (23,297 ) Earnings per share: Basic $ 0.57 $ (3.65 ) Diluted $ 0.55 $ - Weighted average number of shares used in calculation: Basic 7,272,364 6,383,956 Diluted 7,423,936 6,383,956 (4) Some items in the prior year financial statements were reclassified to conform to the current presentation. Reclassification had no effect on the prior year net income or shareholders equity. America's Car-Mart, Inc. Condensed Consolidated Balance Sheet and Other Data (Amounts in thousands, except per share data) October 31, April 30, October 31, 2024 2024 2023 Cash and cash equivalents $ 8,006 $ 5,522 $ 4,313 Restricted cash from collections on auto finance receivables $ 121,678 $ 88,925 $ 90,180 Finance receivables, net $ 1,132,618 $ 1,098,591 $ 1,105,236 Inventory $ 122,102 $ 107,470 $ 113,846 Total assets $ 1,575,176 $ 1,477,644 $ 1,487,149 Revolving lines of credit, net $ 107,365 $ 200,819 $ 165,509 Notes payable, net $ 656,414 $ 553,629 $ 579,030 Treasury stock $ 298,198 $ 297,786 $ 297,489 Total equity $ 553,665 $ 470,750 $ 476,609 Shares outstanding 8,253,186 6,394,675 6,392,838 Book value per outstanding share $ 67.13 $ 73.68 $ 74.62 Allowance as % of principal balance net of deferred revenue 24.72 % 25.32 % 26.04 % Changes in allowance for credit losses: Six months ended October 31, 2024 2023 Balance at beginning of period $ 331,260 $ 299,608 Provision for credit losses 194,945 231,718 Charge-offs, net of collateral recovered (189,512 ) (186,996 ) Balance at end of period $ 336,693 $ 344,330 America's Car-Mart, Inc. Condensed Consolidated Statements of Cash Flows (Amounts in thousands) Six Months Ended October 31, 2024 2023 Operating activities: Net (loss) $ 4,135 $ (23,277) Provision for credit losses 194,945 231,718 Losses on claims for accident protection plan 16,797 15,173 Depreciation and amortization 3,810 3,389 Finance receivable originations (527,487) (580,082) Finance receivable collections 224,640 218,208 Inventory 48,141 65,123 Deferred accident protection plan revenue (880) 1,306 Deferred service contract revenue (13,300) 4,042 Income taxes, net (974) (8,605) Other 12,967 (3,125) Net cash used in operating activities (37,206) (76,130) Investing activities: Purchase of investments (9,865) - Purchase of property and equipment and other 24 (1,588) Net cash used in investing activities (9,841) (1,588) Financing activities: Change in revolving credit facility, net (93,127) (2,152) Payments on notes payable (345,622) (250,935) Change in cash overdrafts 2,074 1,416 Issuances of notes payable 449,889 360,340 Debt issuance costs (4,467) (4,091) Purchase of common stock (412) (69) Dividend payments (20) (20) Exercise of stock options and issuance of common stock 73,969 (312) Net cash provided by financing activities 82,284 104,177 Increase in cash, cash equivalents, and restricted cash $ 35,237 $ 26,459 America's Car-Mart, Inc. Reconciliation of Non-GAAP Financial Measures (Amounts in thousands) Calculation of Debt, Net of Total Cash, to Finance Receivables: October 31, 2024 April 30, 2024 Debt: Revolving lines of credit, net $ 107,365 $ 200,819 Notes payable, net 656,414 553,629 Total debt $ 763,779 $ 754,448 Cash: Cash and cash equivalents $ 8,006 $ 5,522 Restricted cash from collections on auto finance receivables 121,678 88,925 Total cash, cash equivalents, and restricted cash $ 129,684 $ 94,447 Debt, net of total cash $ 634,095 $ 660,001 Principal balance of finance receivables $ 1,473,794 $ 1,435,388 Ratio of debt to finance receivables 51.8 % 52.6 % Ratio of debt, net of total cash, to finance receivables 43.0 % 46.0 % Three Months Ended Six Months Ended October 31, October 31, Calculation of Adjusted Gross Margin 2024 2024 Sales (A) $ 285,774 $ 573,022 Less: Service contract adjustment to sales (13,181 ) (13,181 ) Adjusted sales (B) 272,593 559,841 Cost of sales (C) (173,215 ) (359,785 ) Gross margin (A-C) $ 112,559 $ 213,237 Adjusted gross margin (B-C) $ 99,378 $ 200,056 Gross margin as a % of sales (A-C/A) 39.4 % 37.2 % Adjusted gross margin as a % of sales (B-C/B) 36.5 % 35.7 % Three Months Ended October 31, Calculation of Adjusted Earnings (Loss) Per Share 2024 Net income attributable to common shareholders (D) $ 5,089 Service contract adjustment to sales (E) 13,181 Credit loss impact of adjustment (F) (3,258 ) Pre-tax impact of adjustment (G) 9,923 Tax effect of adjustment (effective tax rate of 28.34%) (H) (2,812 ) Post-tax impact of adjustment (G+H) 7,111 Adjusted net income (loss) attributable to common shareholders (D-(G+H)) (2,022 ) Weighted average diluted shares outstanding 8,292 Adjusted (loss) per share $ (0.24 ) Diluted earnings per share (GAAP) $ 0.61 Diluted earnings per share impact of adjustment $ 0.85 Photos accompanying this announcement are available at

https://www.globenewswire.com/NewsRoom/AttachmentNg/bfa42c2b-4e44-470f-b96c-6776ace16f96

https://www.globenewswire.com/NewsRoom/AttachmentNg/c8a31827-6416-4053-8972-c8a103a202c8

https://www.globenewswire.com/NewsRoom/AttachmentNg/3ccc7626-309a-4fd6-a2cd-e41d3ee4bc91

Revenue & Gross Margin Chart

Revenue & Gross Margin Chart

Average Retail & Ancillary Chart

Average Retail & Ancillary Chart

SG&A and Net Charge Offs Chart

SG&A and Net Charge Offs Chart